Created in 2006, Spuerkeess Asset Management S.A. (Spuerkeess AM) is an independent asset management company whose shareholder is Banque et Caisse d'Epargne de l'Etat, Luxembourg (Spuerkeess) which holds 100% of the shares. With a multidisciplinary team of more than 20 employees, Spuerkeess AM is managed by Hélène Corbet and Carlo Stronck.

EUR 4 billion assets under management

Spuerkeess AM currently manages more than 30 sub-funds (lux|funds and third party funds) and institutional portfolios for a total amount of more than EUR 4.0 billion in net assets. The funds under management cover all traditional asset classes such as equities, bonds, money market instruments and funds of funds.

The management company also acts as an advisor for a private bank and manages several institutional mandates on behalf of national and international companies, as well as public and para-public institutions. The portfolios include the management of discretionary mandates, pension funds and white label investment funds.

Reassuring asset management

As the objective is to obtain regular capital growth and/or stable and recurring income, Spuerkeess AM's investment culture can be qualified as dynamically conservative.

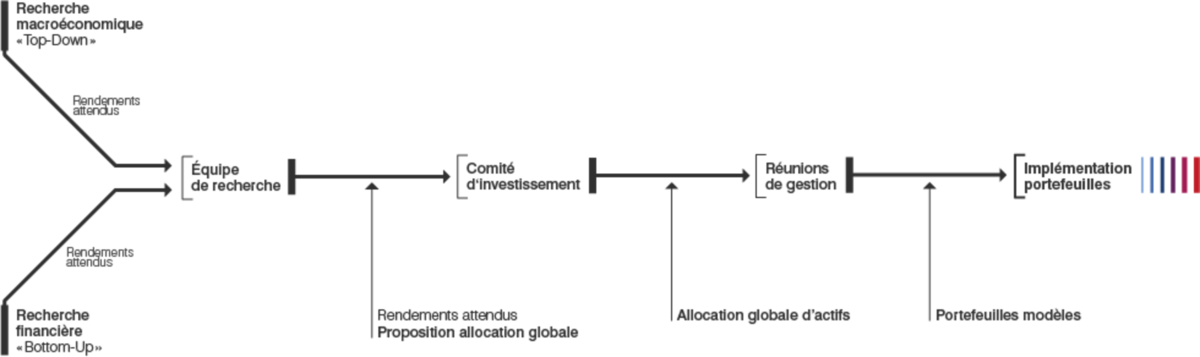

In the initial phase, a research team made up of Spuerkeess AM economists, strategists, analysts and managers defines expected returns by asset class and a global allocation portfolio for an average risk level (neutral allocation).

On the basis of proposals issued by the research team, the investment committee then approves the global allocation used to define the different portfolios according to separate risk constraints.

The selection of shares is based on a Spuerkeess AM-specific approach, the S-GARP (Sustainable Growth At a Reasonable Price), which enables us to avoid traditional pitfalls during market phases, significantly favouring one style at the expense of the other. Moreover, the absolute performance of the investments made via this approach is less dependent on market cycles and the investments have lower volatility for a given performance.

Similar to the S-GARP securities selection process for equities, the S-QARP approach (Sustainable Quality At a Reasonable Price) is used for selecting bonds by putting the emphasis on "sustainable quality".